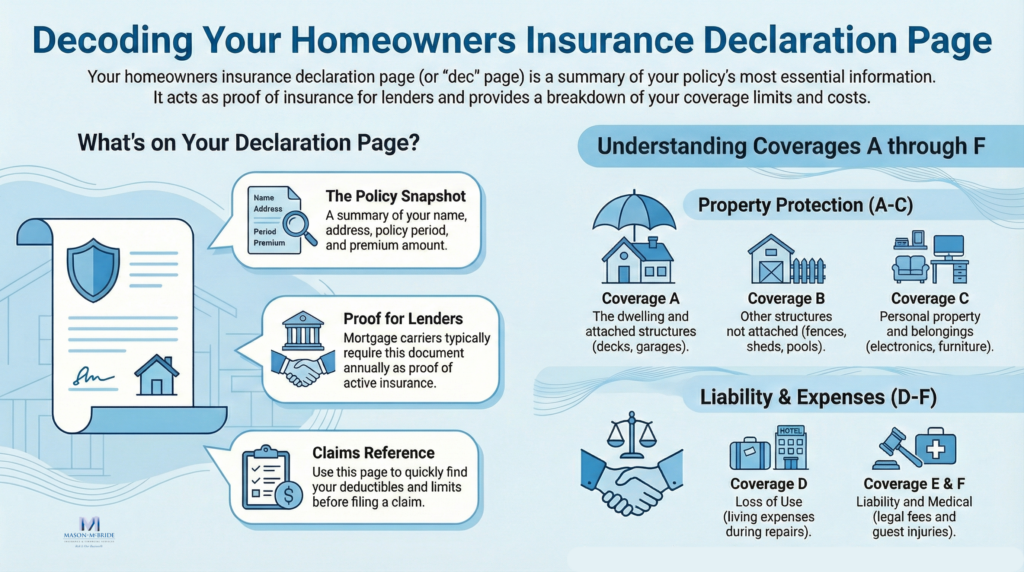

Your homeowners insurance declaration page, often called the “dec” page, summarizes the essential information about your insurance coverage.

This document is critical as it acts as proof of insurance for mortgage lenders and gives you a quick overview of your policy’s details.

We’re here to break down the insurance jargon so you can confidently read your declaration page and understand how your policy protects your home.

What Is a Home Insurance Declaration Page?

A homeowners’ insurance declaration page is a document provided by your insurance carrier that outlines key details of your policy. It includes your name, address, insured property description, premium, coverages, limits, deductibles, discounts, policy forms, and endorsements.

Mortgage carriers typically require this document as proof of insurance each year. It’s also helpful when considering whether to file a claim, as it summarizes your policy’s basic coverages and limits.

Where to Find Your Insurance Declaration Page

When you purchase home insurance, your carrier typically will automatically send your declaration page, usually at the beginning of your policy documents. You may receive it by email, mail, or through your insurer’s online portal.

If you can’t find your declaration page, you can request a copy from your insurance provider or download it from their website if available.

What’s Included on the Declaration Page?

At the top of your declaration page, you’ll see your policy number and the policy period (the duration of your coverage). Your name will be listed as the insured, along with the name of your agent or agency and the insurance carrier.

The page also typically includes:

- The insured property’s address

- Your premium amount

- Coverages and their limits

- Deductibles

- Discounts or credits

- Any endorsements or riders

Understanding Homeowners Insurance Coverages

Homeowners’ insurance policy includes several types of coverage, often labeled A through F:

- Coverage A: Dwelling

Covers the structure of your home, including anything physically attached (e.g., deck, garage, patio). - Coverage B: Other Structures

Covers buildings not attached to your home, such as fences, sheds, pools, or gazebos. - Coverage C: Personal Property

Covers your belongings (furniture, electronics, etc.). High-value items like jewelry may have sub-limits. You may need additional coverage (riders) for full protection. - Coverage D: Loss of Use

Pays for living expenses if you need to stay elsewhere during repairs for a covered claim. - Coverage E: Personal Liability

Provides legal protection if you’re sued for an accident on your property. - Coverage F: Medical Payments to Others

Covers medical costs if someone is injured on your property, up to a certain amount.

Policy Endorsements & Riders

Endorsements (or riders) are optional additions that modify your policy, providing extra coverage or specifying exclusions. For example:

- Jewelry, watches, or fine art: Standard policies limit coverage for valuable items. Scheduling these items as riders ensures full protection.

- Water/Sewer Backup: Protects against damage from backup of water or materials from a sewer, sump pump, or drain.

Common Policy Types:

- HO-3: Basic homeowners policy with named perils coverage.

- HO-5: Broader, open-peril coverage for home and contents.

- HO-4: Renters insurance (covers belongings and liability).

It’s helpful to know what your policy doesn’t cover. Standard home insurance typically does not cover events like flooding, earthquakes, or sewer backup unless you’ve added specific endorsements.

How to Use Your Declaration Page

- Review for accuracy: Check names, addresses, coverage limits, discounts, and endorsements.

- Use as proof of insurance: Mortgage lenders may request your dec page.

- Refer to it when filing a claim: Keep your policy number handy.

- Contact your agent or insurer if you notice errors or need clarification.

Frequently Asked Questions

- Can the declaration page be used as proof of insurance?

Yes, it’s commonly accepted by lenders. - Will I get a new dec page if I change my policy?

Yes, any updates or changes will generate a new declaration page. - What’s the difference between a declaration page and a certificate of insurance?

The declaration page provides more detail and is primarily for your reference, while a certificate of insurance is a brief summary for third parties.

Final Thoughts and Next Steps

Your homeowners insurance declaration page is a vital document that summarizes your coverage, limits, deductibles, and endorsements. Understanding it ensures you get the benefits you paid for and know what’s excluded.

If you’re unsure about any aspect of your home insurance policy, don’t hesitate to reach out to Mason-McBride for clarification.

Get More Answers

Have questions about your coverage? Talk with an independent agent at Mason-McBride or get a quote started.

For helpful tips on other popular insurance topics, check out articles on: