Insurance costs have increased steadily over the past several years, and many policyholders are feeling the impact.

While inflation is a contributing factor, the broader issue is a prolonged hard market that affects pricing, availability, and underwriting scrutiny across nearly every line of insurance, including home insurance and auto insurance.

According to recent industry reports, the combination of economic pressure, loss severity, and elevated reinsurance costs has created some of the most challenging conditions the market has seen in more than a decade.

Why Insurance Rates Are Going Up?

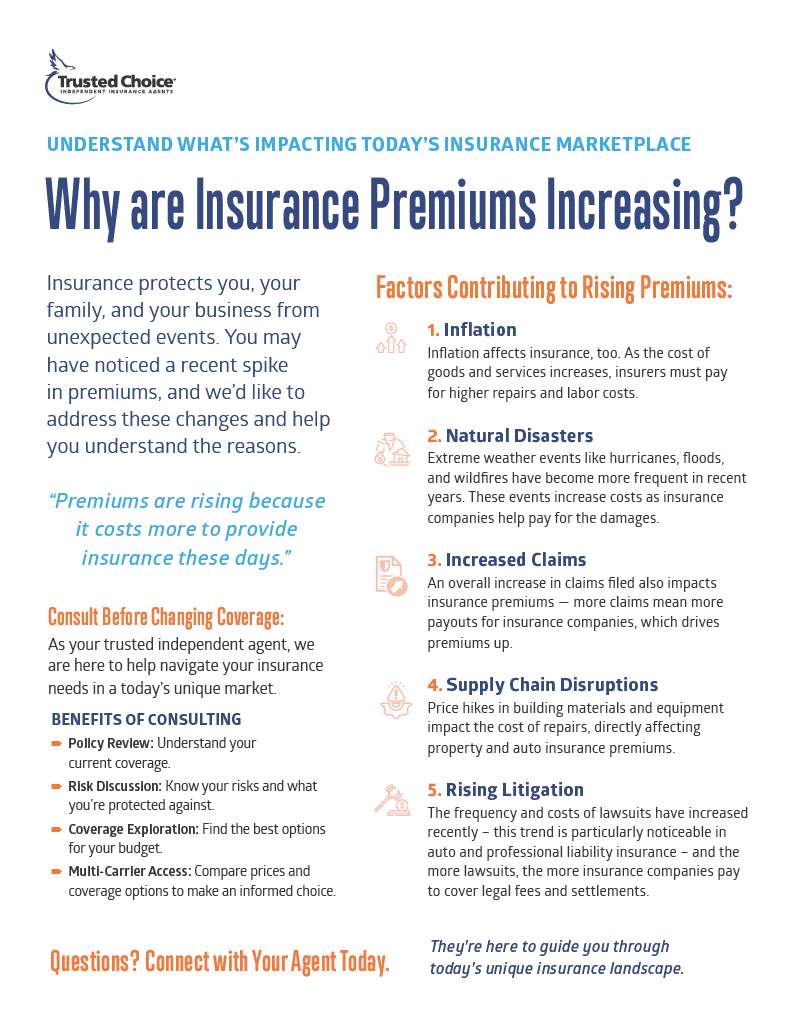

Insurance premiums are increasing primarily due to:

- Rising repair and construction costs caused by inflation

- More frequent and severe weather-related losses

- Increased claim severity and settlement costs

- Supply chain disruptions impacting repairs

- Higher reinsurance and litigation expenses

These factors affect the entire insurance industry, meaning premiums may increase even for policyholders with no claims history.

What Is an Insurance Hard Market?

An insurance hard market is a period when insurance becomes more expensive and harder to obtain because insurers are working to manage higher financial risk.

| Market Change | What Happens | Policyholder Impact |

|---|---|---|

| Higher Pricing | Premiums increase across most policies | Larger renewal increases |

| Stricter Underwriting | Greater risk evaluation | Inspections and updates required |

| Reduced Carrier Appetite | Insurers limit higher-risk policies | Fewer coverage options |

| Limited Capacity | Less competition among insurers | Pricing flexibility decreases |

Remember:

- Your specific risk: Your location, and other factors can influence your premium more during a hard market.

How These Conditions Affect Policyholders

- Limited Coverage Options: During a hard market, insurance companies may reduce the types of risks they are willing to insure. Fewer carriers competing in the marketplace can make coverage more difficult to place in certain situations.

- Stricter Inspections: Insurers often require more detailed underwriting reviews and property inspections. Previously unnoticed maintenance issues may need to be addressed to maintain coverage.

- Premium Increases: Higher material, labor, and repair costs require insurers to adjust coverage limits and premiums to keep pace with rising replacement values.

- Risk of Underinsurance: If coverage limits have not been updated to reflect current rebuilding or replacement costs, policyholders may face gaps in protection following a loss.

Frequently Asked Questions About Rising Insurance Costs

Why did my insurance premium increase even though I haven’t had a claim?

Individual claims history is only one factor in pricing. Insurance premiums are also influenced by broader market conditions, including inflation, catastrophe losses, and rising repair costs affecting the entire industry.

When will insurance rates go back down?

Insurance markets are cyclical. Hard markets typically last several years and begin to ease as economic conditions stabilize, competition increases, and loss trends improve. The timing varies depending on industry and economic factors.

Communicating with Your Insurance Agent

Navigating a hard market can be challenging. Open communication with your agent is crucial. They can help you:

- Understand how home insurance and auto insurance premiums are affected

- Adjust coverage to avoid underinsurance

- Explore discounts and endorsements to manage costs

By staying proactive and informed, you can make smart decisions to protect your assets during a hard market.

Related Insurance Resources

These guides may help you better understand your coverage:

- Extra Protection Beyond Home & Auto Insurance

- Understanding Your Home Insurance Declaration Page

- Insuring Your Home: Replacement Cost vs. Market Value

- Personal Injury Protection & Qualified Health Letters

Article By: Karly Smith